阅读:0

听报道

推文人 | 苏应俊 葛梦君

原文信息:Daniel Ackerberg & Garth Frazer & Kyoo il Kim & Yao Luo & Yingjun Su, 2020. "Under-Identification of Structural Models Based on Timing and Information Set Assumptions."Available at SSRN:

前言

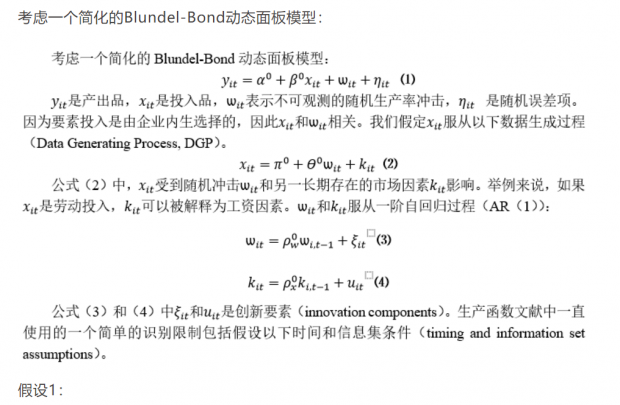

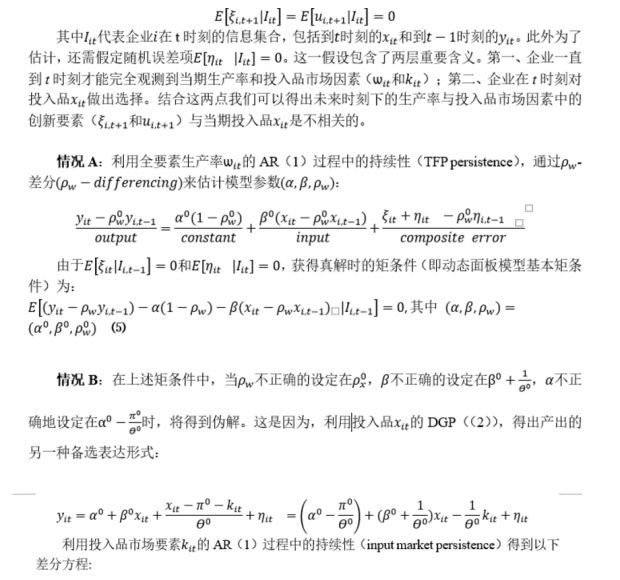

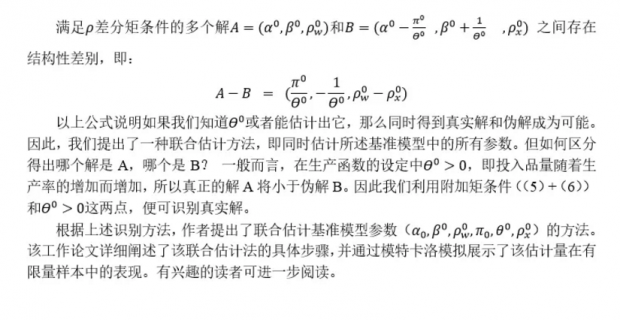

由于不可观测的生产率与企业的要素投入之间的相关性,在存在内生性问题的情况下如何对生产函数进行估计是产业经济学领域最为前沿的热点问题之一。目前常用的两种生产函数估计法为代理变量法(proxy variable approach)和动态面板法(dynamic panel approach)。然而,面对生产函数系数估计,你是否有过以下疑惑?通过广义矩估计得到的生产函数系数似乎与经济理论或者产业技术建议的参数范围不一致;或者出现模棱两可的情况,即运用同一矩估计却得到了多组均能解释数据的系数。如果你也被类似问题困扰过,你并非孤身一人!本文用一个简化的Blundel-Bond动态面板模型演示了为什么会出现这样的问题,并且提供了简易可行的一般解决方案来去伪存真。

可能存在的一矩多解问题

解决方案

更多一般经验

在前面的内容中,作者提供了改进的估计方法以避免出现伪解,但该方法适用于特殊设定下的模型。以下,我们提供在更一般的情况下去伪存真的几种方法。

1. 研究者可根据具体研究问题和背景指定厂商对投入品的选择过程(DGP),并按照前面的逻辑推导出类似的附加矩条件估计法。

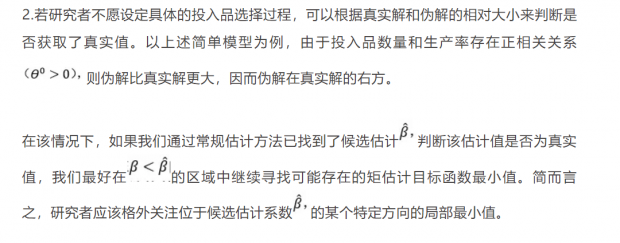

3.研究者可先按照常规的估计流程获取候选估计系数,通过对生产率估计值与投入品数量的相关关系做事后检验来判断系数真伪。举例来说,若在模型设定中,我们认为生产率与投入品数量存在正相关关系,而由候选估计系数还原的生产率估计值与投入品量却存在负相关关系,则该候选值可能为伪解。

4.研究者可先设定更强的时间或信息集合假设,在该模型框架下对生产函数进行估计,用得到的系数作为起始值对更一般的(正确)模型进行估计。尽管该强假设下的模型可能并非正确的模型,但该模型本身不会出现伪解,因此以该模型得到的解为初始估计值有助于降低在正确模型中得到伪解的可能性。

当然,上述建议在避免出现伪解的问题上并非万无一失。另外,在一些更复杂的模型(例如设定更强的时间或信息集合假设),甚至可能不存在伪解。但我们认为意识到生产函数估计可能出现伪解,以及掌握避免伪解出现的方法,对研究者来说具有很高的实用价值。

Abstract

We revisit identification based on timing and information set assumptions in structural models, which have been used in the context of production functions, demand equations, and hedonic pricing models (e.g. Olley and Pakes (1996), Blundell and Bond (2000)). First, we demonstrate a general under-identification problem using these assumptions, illustrating this with a simple version of the Blundell-Bond dynamic panel model. In particular, the basic moment conditions can yield multiple discrete solutions: one at the persistence parameter in the main equation and another at the persistence parameter governing the regressor. Second, we propose possible solutions based on sign restrictions and an augmented moment approach. We show the identification of our approach and propose a consistent estimation procedure. Our Monte Carlo simulations illustrate the under-identification issue and finite sample performance of our proposed estimator. Lastly, we show that the problem persists in many alternative models of the regressor but disappears in some models under stronger assumptions.

话题:

0

推荐

财新博客版权声明:财新博客所发布文章及图片之版权属博主本人及/或相关权利人所有,未经博主及/或相关权利人单独授权,任何网站、平面媒体不得予以转载。财新网对相关媒体的网站信息内容转载授权并不包括财新博客的文章及图片。博客文章均为作者个人观点,不代表财新网的立场和观点。

京公网安备 11010502034662号

京公网安备 11010502034662号 {kind=link}