阅读:0

听报道

推文人 | 杨冬

推文信息:Asgharian H , Hou A J , Javed F . The Importance of the Macroeconomic Variables in Forecasting Stock Return Variance: A GARCH-MIDAS Approach[J]. Journal of Forecasting, 2013, 32(7):600-612.

研究介绍

近些年来,对于时变波动率的预测已经得到了长足的进展,如ARCH模型和SV模型。但对于股票波动具有时变性的原因仍然未有定论。本文采用了一种与以往不同的方法,将日度股票市场数据与月度或季度宏观经济变量相结合,构建了混频数据抽样-广义自回归条件异方差(MIDAS-GARCH)模型。

模型设定

实证建模

本文使用了美国日度股票收益率进行分析。在条件方差设定中,文中作者使用了一系列被认为对收益率方差具有影响的金融和宏观经济因子。具体包括:(1)短期利率;(2)收益率曲线斜率;(3)违约率;(4)汇率;(5)通货膨胀率;(6)经济增长率;(6)失业率。数据跨度为1991年1至2008年6月。

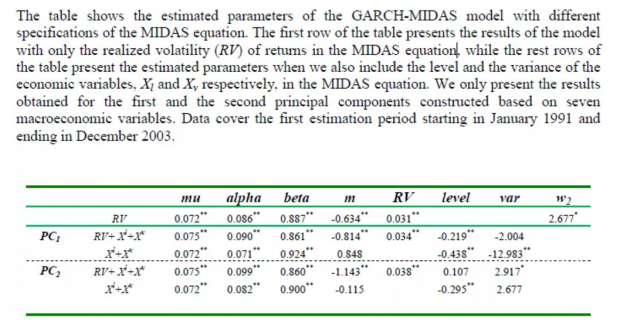

在模型设定方面,作者在长期成分部分分别考虑了三种设定形式:

1.已实现波动率模型:仅使用月度已实现波动率构建MIDAS方程;

2.已实现波动率模型+宏观经济变量水平值+宏观经济变量方差:这一设定可以方便识别宏观因子和月度已实现波动率中的信息。

3.宏观经济变量水平值+宏观经济变量方差:这一设定中,我们仅考虑宏观经济变量的影响。

由于GARCH-MIDAS模型的设定较为复杂,增加了模型的计算难度,为了保证模型的可识别性和避免收敛问题。文中作者采用了主成分分析方法,将宏观经济变量进行了压缩。

上表中给出了GARCH-MIDAS模型的估计结果。由表中结果可知,短期方差成分g在大部分条件下显著,意味着短期收益率方差具有波动聚集性;在长期方差成分方面,参数同样显著。同时可以发现,RV含有主成分1中的部分信息,但主成分1和主成分2含有的信息可以解释股票市场的方差。

结论

本文使用了GARCH-MIDAS方法对方差进行了建模。为了估计方差中的长期成分,通过主成分方法的使用,将多个宏观经济变量进行了汇总,使用其来估计已实现波动率。实证结果表明,GARCH-MIDAS模型在样本内和样本外均具有良好的表现。

Abstract

This paper aims to examine the role of macroeconomic variables in forecasting the return volatility of the US stock market. We apply the GARCH-MIDAS (Mixed Data Sampling) model to examine whether information contained in macroeconomic variables can help to predict short term and long-term components of the return variance. We investigate several alternative models and use a large group of economic variables. A principal component analysis is used to incorporate the information contained in different variables. Our results show that including low frequency macroeconomic information into the GARCH-MIDAS model improves the prediction ability of the model, particularly for the long-term variance component. Moreover, the GARCH-MIDAS model augmented with the first principal component outperforms all other specifications, indicating that the constructed principal component can be considered as a good proxy of the business cycle.

话题:

0

推荐

财新博客版权声明:财新博客所发布文章及图片之版权属博主本人及/或相关权利人所有,未经博主及/或相关权利人单独授权,任何网站、平面媒体不得予以转载。财新网对相关媒体的网站信息内容转载授权并不包括财新博客的文章及图片。博客文章均为作者个人观点,不代表财新网的立场和观点。

京公网安备 11010502034662号

京公网安备 11010502034662号 {kind=link}